You may be thinking about refinancing this year to take advantage of falling interest rates. Or you may have refinanced your home mortgage last year and have yet to file your 2018 return (because you filed an extension). Either way, there are important federal income tax implications. Here's what you need to know.

Deductions for Home Mortgage Interest

For federal income tax purposes, you can deduct interest on a mortgage that qualifies as home acquisition debt. In addition, you can deduct or amortize points paid to take out a mortgage that qualifies as home acquisition debt.

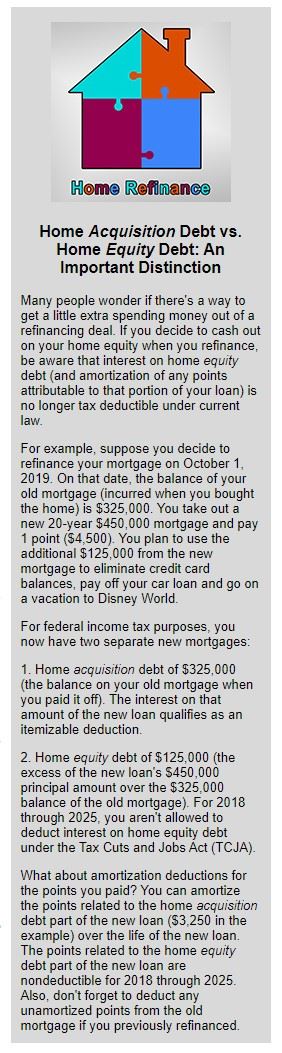

However, for 2018 through 2025, the Tax Cuts and Jobs Act (TCJA) reduced the amount that can be treated as tax-favored home acquisition debt to $750,000 (or $375,000 if you use married filing separately status).

Fortunately, these reduced limits apply in a refinancing context only if you refinance a loan that was taken out after December 15, 2017. If you refinance a loan that was taken out on or before that date, or one that was subject to a binding contract on or before that date, the new loan is grandfathered in under prior law. That means the new loan is subject to the more-generous pre-TCJA home acquisition debt limit of $1 million (or $500,000 if you use married filing separately status).

So, if you refinance an older home acquisition loan, the more-generous limits will apply, and you can potentially treat that much of the refinanced loan balance as tax-favored home acquisition debt. Plus, you can potentially deduct or amortize the related refinancing points as well.

Important Caveat

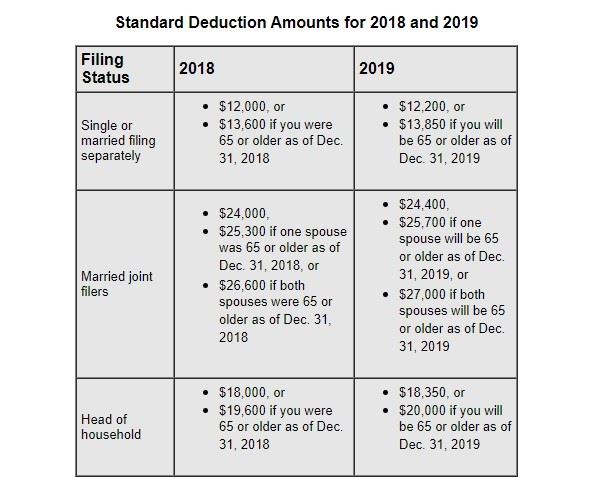

The word "potentially" applies because you don't get any tax benefit from mortgage interest or refinancing points unless you itemize. For 2018 through 2025, fewer taxpayers will be itemizing, because the TCJA increased the standard deduction amounts as follows:

These higher standard deduction amounts under the TCJA reduce the chance that you'll itemize deductions and gain any tax savings from refinanced mortgage interest or refinancing points.

Deductions for Refinancing Points

Deductions for Refinancing Points

Assuming that you itemize deductions, points paid to refinance the remaining balance of your old loan must be amortized over the new loan's life.

For example, Al refinanced his old mortgage on July 1, 2019. He paid $6,000 in points for a new 15-year mortgage (180 months) with the same principal balance as his old loan.

Al can amortize the points over the life of the new loan. For 2019, his amortization deduction will be $200 ($6,000 divided by 180 months times 6 months). His amortization deductions will continue in 2020 and beyond, at the rate of $33.33 per month ($400 per year), for as long as the new loan remains outstanding.

In addition, he can currently deduct refinancing points to take out additional mortgage debt that qualifies as home acquisition debt because it's used to finance improvements to his residence.

Barb's old mortgage was for $400,000. She refinanced her home in 2019 with a new 15-year mortgage for $600,000. Barb spent the additional $200,000 to add a family room and remodel the kitchen. She also paid 1 point ($6,000) to get the new loan.

Barb can immediately deduct one-third ($200,000 divided by $600,000) of the refinancing points, or $2,000, on her 2019 return as long as she paid at least that amount out-of-pocket to get the new loan.

For the remaining two-thirds ($400,000 divided by $600,000) of the refinancing points, or $4,000, Barb can claim amortization deductions over the new loan's 15-year term (180 months). So, she can deduct $22.22 ($4,000 divided by 180 months) for each month the new loan is outstanding during 2019. In 2020 and beyond, she can continue claiming amortization deductions of $22.22 per month for as long as the new loan remains outstanding.

Important: If you roll all the refinancing costs, including the points, into the balance of the new loan, you must amortize the entire amount of the points over the term of the new loan. So, there would be no current deduction in this scenario.

Deductions for Unamortized Points from Prior Refinancing

If you've previously refinanced your home and paid points, you may have an unamortized (not-yet-deducted) balance remaining. There's good news: You can probably deduct that entire unamortized amount when you refinance again.

For example, Charlie is a serial refinancer. He refinanced his mortgage in 2014 and then again in 2019. In 2014, Charlie took out a 30-year loan for $450,000 and paid 1 point ($4,500). He has $3,750 of unamortized (not-yet-deducted) points left over from the earlier refinancing loan. Assuming Charlie itemizes expenses for 2019, he can deduct the unamortized point ($3,750), along with any deductible interest and amortization for points paid on the new loan.

Got Questions?

The tax implications of refinancing your home mortgage are complicated — and they've temporarily gotten less favorable under the TCJA. Contact your tax advisor if you have questions or want more information.

Additional Reading