Do your children or grandchildren receive unearned income from investments? Federal tax law contains provisions that are designed to prevent high-net-worth individuals from shifting investment income to children and young adults in lower tax brackets to minimize the family's overall tax bill. These so-called "kiddie tax" rules have gone through several changes in recent years. Here's the latest.

Important: For simplicity, throughout this article we use the terms "child" and "children" to apply to both children and young adults who are under age 24 and may be subject to the kiddie tax.

History Lesson

Before the Tax Cuts and Jobs Act (TCJA), the federal kiddie tax rules taxed a portion of an affected child's unearned income — typically from investments — at the parent's marginal federal income tax rate if that rate was higher than the rate the child would otherwise pay.

For 2018 through 2025, the TCJA changed the rules. Under the law, a portion of an affected child's unearned income was taxed at the federal income tax rates paid by trusts and estates.

That change was criticized because it could cause the kiddie tax to be much more expensive for a child with substantial unearned income. Why? Because the trust and estate rates quickly rise to 37% for ordinary income and net short-term capital gains and 20% for net long-term capital gains and qualified dividends.

For trusts and estates, the maximum 37% rate on ordinary income kicks in at the following taxable income levels:

- $12,501 for 2018,

- $12,751 for 2019, and

- $12,951 for 2020.

The thresholds for the maximum 20% federal rate on net long-term capital gains and dividends are close, but not identical, to the preceding numbers.

Current Rules

The Setting Every Community Up for Retirement Enhancement (SECURE) Act became law at the end of 2019. It was mainly intended to expand opportunities for individuals to increase their retirement savings. But Congress also decided that the TCJA change to the kiddie tax rates unfairly increased the federal income tax bills of certain children and young adults, including those who are survivors of deceased military personnel, first responders and emergency medical workers. So, the SECURE Act effectively provides a retroactive repeal of the TCJA change to the kiddie tax rates.

The SECURE Act reinstated the pre-TCJA kiddie tax calculation so that it's once again based on the parent's marginal federal income tax rate. The repeal can be a significant tax-saver for children and young adults with substantial investment income.

Important: The SECURE Act only changed the kiddie tax rate structure. All the other kiddie tax rules are the same as before.

The SECURE Act's favorable change to the kiddie tax rates is generally effective for 2020 and beyond. However, you can choose to apply the tax-saving change to 2018 and/or 2019 federal income tax returns.

If a member of your family was subject to the kiddie tax rules, you might want to file amended federal income tax returns for 2018 and 2019. (However, you may not have filed your 2019 return yet, if you extended the due date to October 15.)

The Basics

Under the current kiddie tax rules, a portion of a child's net unearned income can be taxed at the marginal federal income tax rate paid by the child's parent. This is unfavorable, because parents are usually in much higher tax brackets. While the kiddie tax hit on a child with substantial unearned income can be significant, it's lower than before the favorable SECURE Act change.

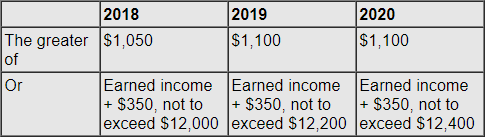

In calculating the federal income tax bill for a child who's subject to the kiddie tax, the child is allowed to subtract his or her standard deduction amount. The following table summarizes the standard deductions for an unmarried dependent child for 2018 through 2020.

Standard Deductions for Unmarried Dependent Child for 2018 – 2020

Age is a key factor in assessing exposure to the kiddie tax. (See "The Age Factor" above.)

Calculating the Kiddie Tax

To calculate the amount of kiddie tax owed, start by adding the child's net earned income (from a part-time job) to his or her net unearned income. Then subtract the applicable standard deduction to arrive at taxable income.

The portion of taxable income that consists of net earned income is taxed at the regular rates for a single taxpayer (assuming unmarried status). The child will owe kiddie tax on the portion of taxable income that consists of net unearned income in excess of the unearned income threshold of:

- $2,100 for 2018, and

- $2,200 for 2019 and 2020.

That excess amount is taxed at the higher of:

- The parent's marginal federal income tax rate, or

- The child's normal federal income tax rate(s).

The applicable rate can be as high as 37% for ordinary income and net short-term capital gains and 20% for net long-term capital gains and qualified dividends.

For example, Inez was 16 years old in 2019. In 2019, she reported $5,000 of earned income from working at a summer camp and $17,000 of unearned income from short-term capital gains from investments held in a custodial account that was set up for her. How much federal income tax would she owe for 2019, assuming her parents are in the 24% marginal federal income tax bracket?

Inez's standard deduction for 2019 is $2,550 ($2,200 of earned income + $350). So, her taxable income is $19,450 ($5,000 + $17,000 − $2,550).

Of that amount, $14,800 ($17,000 − $2,200 unearned income threshold) is subject to the kiddie tax and is therefore taxed at her parents' marginal federal income tax rate of 24%. The remaining $4,650 ($19,450 − $14,800) is taxed at the regular rates for a single taxpayer. The entire $4,650 falls within the 10% federal income tax bracket.

Taking advantage of the retroactive SECURE Act change to the kiddie tax rates, Inez's 2019 federal income tax bill is $4,017. That number is comprised of $3,552 of kiddie tax on her unearned income ($14,800 × 24%), plus $465 of regular tax on her earned income ($4,650 × 10%). Her tax bill would have been even higher if the unfavorable TCJA kiddie tax rate structure was used for the calculation.

Without the kiddie tax, all of Inez's $19,450 of 2019 taxable income would have been taxed at the 10% and 12% rates under the rate structure for single taxpayers.

Need Help?

The kiddie tax rules are still unfavorable. But the SECURE Act change has softened the blow for many affected children and young adults. Contact your tax advisor if you have questions about the kiddie tax or want more information about whether it applies to someone in your family.