Form 706 vs. Form 1041

When a loved one passes away, the executor of the deceased person's estate is charged with handling the estate's financial affairs. If a loved one dies without a valid will, the probate court will appoint an "administrator" to handle these chores. Here's an overview of the tax forms (Form 706 and Form 1041) that may need to be filed for the estate, along with other tax-related issues to consider.

We have the legal solutions you need. Contact Ferrari Ottoboni Caputo & Wunderling LLP at (800) 761-0432 to schedule a consultation today.

What Is Form 1041?

"U.S. Income Tax Return for Estates and Trusts"

Form 1041 is required if the estate generates more than $600 in annual gross income. After an individual has passed away, income generated by his or her holdings now belongs to the estate, and that income is subject to federal income tax.

The executor is responsible for arranging for filing the annual federal income tax return for the decedent's estate. The estate's initial income-tax year begins immediately after the date of death. The tax year-end can be December 31 or the end of any other month that results in an initial tax period of 12 months or less.

The return is due by the 15th day of the fourth month after the tax year-end (adjusted for weekends and holidays). So for a decedent who dies in 2020, the filing deadline is April 15, 2021, assuming the standard December 31 tax year-end is chosen.

There's no need to file Form 1041 if all the decedent's income-producing assets bypass probate and go directly to the surviving spouse or other heirs by contract or operation of law.

Examples of these assets include:

- Real property that's owned as joint tenants with right of survivorship,

- IRAs and qualified retirement plan accounts that have designated account beneficiaries, and

- Life insurance proceeds paid directly to designated policy beneficiaries.

To clarify, no return is required for an estate with an annual gross income below $600. This provision eliminates the need to file Form 1041 for tiny estates and those that can be wrapped up before $600 of income has accumulated.

What Is Form 706?

"United States Estate (and Generation-Skipping Transfer) Tax Return"

The unified federal estate and gift tax exemption is $11.58 million for people who died in 2020 (up from $11.4 million for people who died in 2019). The exemption amount will be adjusted annually for inflation from 2020 through 2025. In 2026, the exemption is set to return to an inflation-adjusted $5 million, unless Congress extends the more generous exemption.

Important note: When calculating the fair market value of the decedent's estate, don't forget to include life insurance proceeds, even if the money goes directly to designated policy beneficiaries. Life insurance proceeds are generally free of any federal income tax, but the proceeds must be considered for federal estate tax purposes.

An exception to this general rule can apply if the policy beneficiary is the surviving spouse. That's because assets inherited by a surviving spouse (including life insurance payouts) aren't included in the decedent's estate for federal estate tax purposes when the surviving spouse is a U.S. citizen. (See "Unlimited Marital Deduction Provides Relief for Surviving Spouses" at right.)

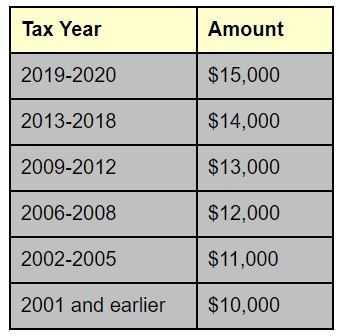

The term "sizable gifts" refers to those in excess of the following amounts to a single recipient in a single year.

If the decedent made any sizable gifts during his or her lifetime, the excess over the applicable threshold for the year of the gift is added back to the estate to determine if the unified federal estate and gift tax exemption is surpassed. If it is, there's a 40% federal estate tax on the excess.

Portability Election

An executor may think Form 706 doesn't need to be filed because no federal estate tax is owed. However, that could be an erroneous conclusion. Filing Form 706 is necessary to make the so-called "portability election."

This election allows the executor to pass the decedent's unused unified federal estate and gift tax exemption to the surviving spouse. The portability privilege can help well-off married couples save significant tax dollars.

When the executor files Form 706 solely to make the portability election, only part of the form must be completed. Plus, an extended filing deadline applies. The deadline is on or before the second anniversary of the decedent's date of death.

Should the executor always file Form 706 to make the portability election? It can't hurt. After all, it's unclear what the allowable unified federal estate and gift tax exemption will be in the future — or if there will even be one.

Also uncertain is the future impact of making an earlier portability election. So, making the election can't possibly hurt, and it might pay off in the future.

Other Tax-Related Loose Ends

If the executor will file Form 1041 and/or Form 706, he or she will first need to obtain a federal employer identification number (EIN) for the estate. The EIN is analogous to an individual's Social Security number.

Next, the executor should file Form 56, "Notice Concerning Fiduciary Relationship," to notify the IRS that the executor will be acting on behalf of the estate regarding federal tax matters. Filing Form 56 helps ensure that the executor will receive any notices sent out by the IRS.

Then, the executor should open a checking account in the name of the estate with some funds transferred from the decedent's accounts. The executor has the legal power to do this. But the bank will require the executor to provide an EIN for the estate.

The executor uses this new account to accept deposits from income earned by the estate and to pay the estate's expenses, such as:

- Medical expenses

- Funeral costs

- Taxes

- And other outstanding bills

Unfortunately, the executor's job still may not be finished. He or she may also be responsible for state income tax returns and (if applicable) a state death tax return.

Need Help?

When a loved one who is financially comfortable passes away, a bevy of tax issues can come into play. The executor is responsible for dealing with those issues, and it can be a daunting task.

Your tax law professional can provide valuable assistance in meeting applicable tax compliance rules and in developing appropriate tax planning strategies for the future.

Our boutique firm is large enough to offer high caliber service, but with a personalized touch. Find out how our tax lawyers can help you by calling us at (800) 761-0432 today or by filling out our online contact form.

Related Reading: